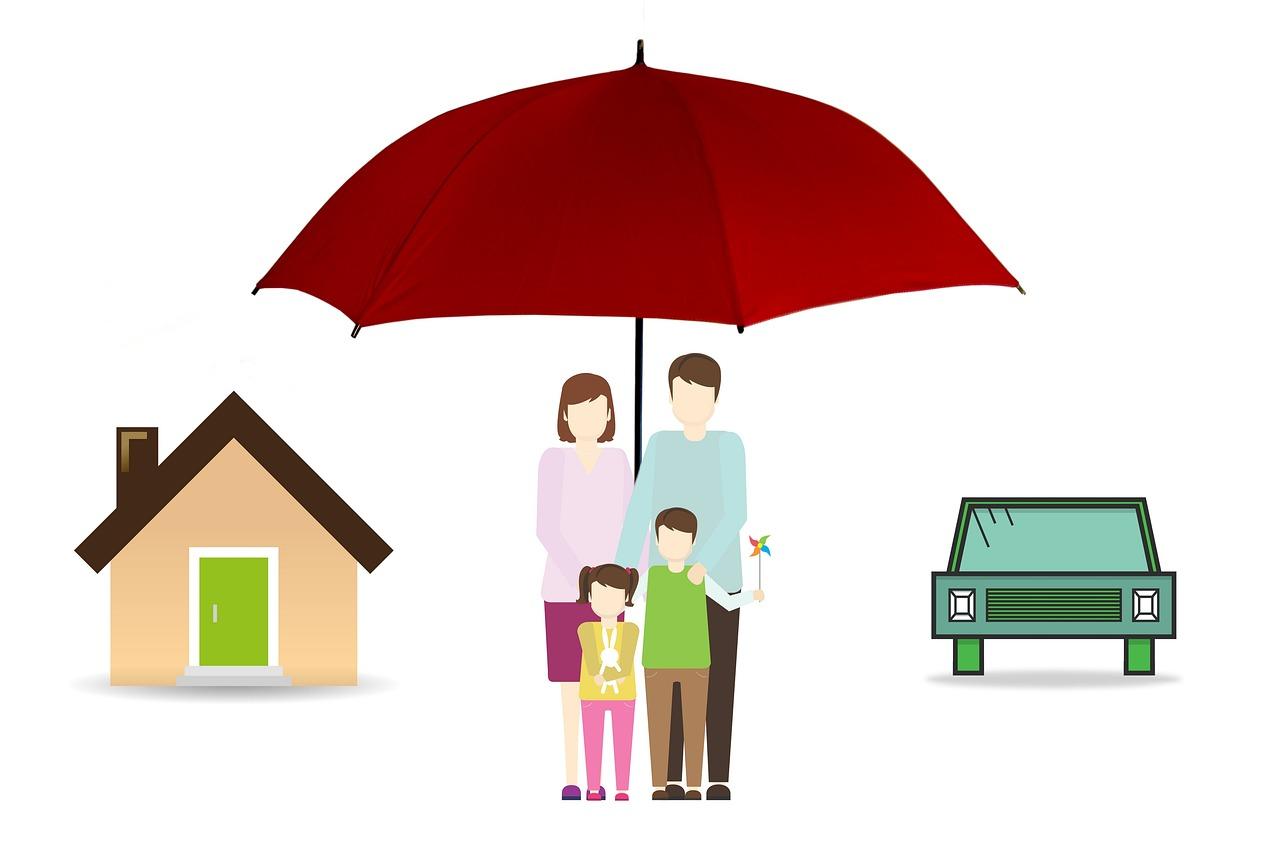

When it comes to protecting our assets and securing peace of mind, insurance often plays a pivotal role in our financial strategy. While most of us are familiar with standard policies like auto, home, and health insurance, there’s another layer of coverage that frequently flies under the radar: umbrella insurance. Designed to provide an extra layer of liability protection beyond what your primary policies offer, umbrella insurance can be a valuable addition for many individuals. But is it worth the investment? In this article, we’ll delve into what umbrella insurance covers, who might benefit from it, and the factors to consider when weighing its value. Whether you’re a homeowner, a renter, or somewhere in between, understanding how this unique form of insurance works can help you make informed decisions about your financial future. Let’s explore the ins and outs of umbrella insurance and determine if it’s a wise choice for your situation.

Table of Contents

- Understanding the Basics of Umbrella Insurance and Its Benefits

- Common Misconceptions Surrounding Umbrella Insurance Coverage

- Determining Your Need for Umbrella Insurance: A Personal Assessment

- What to Consider When Choosing an Umbrella Insurance Policy

- Concluding Remarks

Understanding the Basics of Umbrella Insurance and Its Benefits

Umbrella insurance is designed to provide an additional layer of protection beyond what standard policies, such as auto or homeowners insurance, offer. While these traditional policies have limits on liability coverage, umbrella insurance can kick in once those limits are reached. This means that, in the event of a lawsuit or major claim, you can rest assured knowing your assets are safeguarded. Key benefits of umbrella insurance include:

- Expanded Coverage: It covers claims that may not be included in your regular policies.

- Higher Liability Limits: Offers significant coverage amounts, often starting at $1 million.

- Asset Protection: Shields your savings, properties, and future earnings from potential lawsuits.

One common misconception is that only wealthy individuals require this type of coverage; however, anyone can be vulnerable to a liability claim. Even a minor incident, like a guest slipping and falling on your property, could lead to substantial medical expenses or legal fees. Umbrella insurance is relatively affordable, typically costing only a few hundred dollars per year for substantial coverage. Here are some considerations to keep in mind:

| Consideration | Details |

|---|---|

| Cost | Inexpensive for the level of coverage provided. |

| Eligibility | Usually requires existing home and auto insurance. |

| Peace of Mind | Enhances confidence in your financial security. |

Common Misconceptions Surrounding Umbrella Insurance Coverage

Many people believe that umbrella insurance is unnecessary or only for the wealthy, but this is far from the truth. Umbrella insurance is designed to provide an extra layer of liability protection that can be beneficial for a variety of individuals, regardless of their financial status. It covers various scenarios that are often overlooked, such as personal injury claims, libel, and slander, meaning even those with average incomes can find peace of mind with this policy. Furthermore, it can kick in when other liability limits—like those on your home or auto insurance—have been reached, effectively safeguarding your assets from potential lawsuits.

Another common misconception is that umbrella insurance is complicated and difficult to understand, but many policies are straightforward and easy to navigate. Here are a few key points to demystify the coverage:

- Broad Coverage: Umbrella insurance extends beyond standard policies, covering more than just auto or home-related incidents.

- Affordable Premiums: Contrary to popular belief, the cost of umbrella insurance is often quite low compared to the comprehensive protection it offers.

- Prevents Asset Loss: Umbrella insurance can protect your savings, investments, and even future earnings from potential claims.

Determining Your Need for Umbrella Insurance: A Personal Assessment

When evaluating whether you need umbrella insurance, it’s critical to understand your personal circumstances and risk factors. Begin by assessing your assets, which may include your home, savings, and any investments. Consider the following aspects:

- Net Worth: Sum up all your assets and subtract any debts to determine your net worth.

- Income Level: Higher income can lead to greater liability risks, particularly if you are a professional in a high-stakes industry.

- Family Structure: If you have dependents, their financial security might rely on your income, heightening your need for additional coverage.

Next, evaluate your lifestyle and potential risks that could lead to liability claims. Some factors to consider include:

- Home and Property Ownership: Owning a pool, trampoline, or pets may increase liabilities.

- Public Engagement: If you frequently host events or entertain guests, the risk of accidents occurring on your property rises.

- Your Occupation: Certain professions may expose you to higher legal risks, making umbrella insurance more beneficial.

To help visualize your assessment, you might find this simple table useful:

| Assessment Area | Considerations | Impact on Umbrella Need |

|---|---|---|

| Assets | Net worth, savings | Higher assets increase liability risk |

| Income | Job security, potential claims | Stable income means a need for protection |

| Lifestyle | Pets, homes, and public events | Increased activities lead to higher risk |

What to Consider When Choosing an Umbrella Insurance Policy

When selecting an umbrella insurance policy, it is crucial to evaluate your existing coverage limits. Many standard homeowners and auto policies have liability caps that might not adequately protect your assets in the event of a serious claim. Understanding your current policy limits can help you determine how much additional coverage you need. Consider factors such as your income, net worth, and any potential risks associated with your profession or lifestyle to ensure you choose a policy that provides sufficient protection.

Another important aspect to consider is the scope of coverage offered by different umbrella policies. While most policies cover personal liability in various situations, such as accidents or lawsuits, some may have exclusions or specific conditions. It’s advisable to compare options and read the fine print, ensuring that the policy aligns with your specific needs. Furthermore, take note of the policy limits, pricing, and any deductibles involved to find a balance between affordability and adequate protection. Here’s a brief overview of potential factors to weigh:

| Factor | Considerations |

|---|---|

| Coverage Amount | How much additional coverage do you need? |

| Exclusions | What situations are not covered by the policy? |

| Premium Costs | How does the cost compare to potential risks? |

| Deductibles | What out-of-pocket expenses are required before coverage kicks in? |

Concluding Remarks

exploring the realm of umbrella insurance reveals a nuanced financial tool that can serve as an essential safeguard in our increasingly litigious society. While not everyone may need this additional layer of coverage, understanding your personal risk factors and evaluating your existing policies can help you make an informed decision. Whether you’re a homeowner, a business owner, or simply someone looking to protect your assets, umbrella insurance might just be the peace of mind you didn’t know you needed. Weigh the potential risks against the cost, and you’ll be better equipped to decide if this extra insurance is a worthwhile addition to your financial strategy. As always, consider consulting with an insurance professional to tailor a plan that suits your unique needs. Thank you for joining us on this exploration of umbrella insurance, and we hope it has shed light on whether it’s the right choice for you!