Navigating the world of life insurance can often feel daunting, filled with jargon and intricate policies that can leave even the most diligent consumers scratching their heads. Yet, understanding life insurance is crucial, as it plays a significant role in financial planning and securing your loved ones’ futures. Whether you’re a first-time buyer or looking to reassess your existing policy, grasping the fundamental concepts of life insurance can empower you to make informed decisions. In this article, we’ll break down the key insights you should know, demystifying the types of life insurance, the factors that influence rates, and the benefits it can provide. With the right knowledge, you can approach this essential tool with confidence and clarity, ensuring that you choose the best option for your specific needs.

Table of Contents

- The Basics of Life Insurance and Its Importance

- Types of Life Insurance Policies Explained

- Factors to Consider When Choosing a Life Insurance Policy

- Common Misconceptions About Life Insurance and How to Avoid Them

- Wrapping Up

The Basics of Life Insurance and Its Importance

Life insurance serves as a financial safety net, designed to provide peace of mind during uncertain times. By paying a regular premium, policyholders can ensure that their loved ones are financially protected in the event of their untimely demise. This type of insurance can cover various expenses, such as funeral costs, ongoing living expenses, and any outstanding debts. Furthermore, life insurance can serve as an essential part of a robust financial plan, helping family members maintain their standard of living and securing their future during difficult times.

There are different types of life insurance to consider, each catering to unique needs and preferences. The most common types include:

- Term Life Insurance: Offers coverage for a specific period, typically ranging from 10 to 30 years.

- Whole Life Insurance: Provides lifelong coverage with a cash value component that grows over time.

- Universal Life Insurance: Offers flexible premiums and benefits, allowing policyholders to adjust their coverage as needed.

To better understand how life insurance can fit into your financial strategy, consider the following table:

| Type of Insurance | Coverage Period | Cash Value |

|---|---|---|

| Term Life | Fixed term (e.g., 10, 20, 30 years) | No |

| Whole Life | Lifetime | Yes |

| Universal Life | Lifetime | Yes (flexible) |

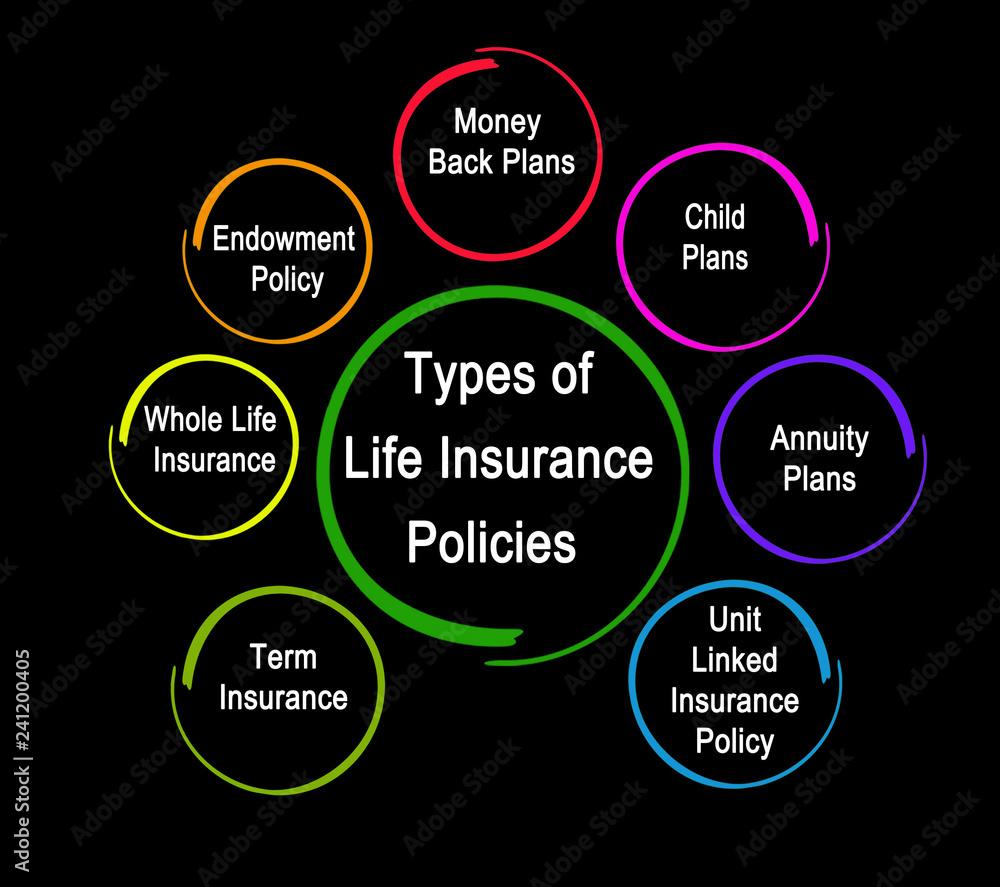

Types of Life Insurance Policies Explained

Life insurance comes in various forms, each tailored to meet different needs and preferences. Understanding these types can help you make an informed decision based on your unique circumstances. Here are some of the most common types:

- Term Life Insurance: This policy provides coverage for a specified term, usually ranging from 10 to 30 years. It offers a death benefit if the insured passes away within that term.

- Whole Life Insurance: A form of permanent insurance that remains in effect for the insured’s lifetime, combining a death benefit with a savings component that grows cash value over time.

- Universal Life Insurance: This flexible policy allows you to adjust your premiums and death benefits, making it suitable for those whose financial situations may change over time.

- Variable Life Insurance: A permanent policy that combines a death benefit with an investment component, allowing policyholders to allocate cash value among a variety of investment options.

To further clarify the distinctions between these policies, here’s a comparison:

| Type | Coverage Duration | Cash Value | Flexibility |

|---|---|---|---|

| Term Life | Fixed Term | No | Low |

| Whole Life | Lifetime | Yes | Low |

| Universal Life | Lifetime | Yes | High |

| Variable Life | Lifetime | Yes | High |

Factors to Consider When Choosing a Life Insurance Policy

Choosing the right life insurance policy involves understanding your unique financial needs and the level of protection you want to provide for your loved ones. Assessing your financial situation is crucial, as it allows you to determine the amount of coverage necessary. Additionally, consider your long-term financial goals, such as paying off debts, funding children’s education, or securing a comfortable retirement. Other essential factors include:

- Your Age and Health Status: Younger individuals often pay lower premiums and may consider longer-term policies.

- Type of Insurance: Decide between term life and permanent life insurance based on affordability and coverage duration.

- Riders and Extra Benefits: Some policies offer additional options like critical illness coverage that can be beneficial.

Another important aspect is the insurance provider’s reputation and financial stability. It’s wise to research the company’s history, customer service record, and claims processing experience. Consider these additional elements when evaluating policies:

- Premium Costs: Ensure that you can comfortably afford the premiums throughout the policy’s term.

- Claims Settlement Ratio: A higher ratio indicates a reliable company that honors claims efficiently.

- Policy Flexibility: Check if the policy allows for adjustments as your circumstances change.

| Type of Policy | Coverage Duration | Typical Use |

|---|---|---|

| Term Life Insurance | 10-30 years | Temporary needs (e.g., mortgages, education) |

| Whole Life Insurance | Lifetime | Permanent coverage and cash value accumulation |

| Universal Life Insurance | Lifetime | Flexible premiums with investment components |

Common Misconceptions About Life Insurance and How to Avoid Them

Many individuals hold on to the misconception that life insurance is only necessary for those with dependents or those who are significantly older. This belief can lead to a significant gap in financial planning for younger individuals or those without children. In reality, life insurance can provide essential financial protection at any age, ensuring that funeral expenses and debts are covered, thereby relieving loved ones of those burdens. Furthermore, purchasing a policy at a younger age often means lower premiums, making it a financially savvy decision.

Another common misunderstanding is that all life insurance policies are the same, leading people to choose the first option they encounter without considering their specific needs. It’s vital to recognize the differences between term and whole life insurance, as well as the varying riders and benefits available. Taking the time to review these options can prevent individuals from inadvertently selecting a policy that doesn’t suit their long-term goals. Key factors to consider include:

- Coverage Amount: Assess how much your loved ones would need in the event of your passing.

- Policy Length: Decide if a term policy or a whole life policy aligns better with your financial strategy.

- Riders: Explore additional features that can enhance your policy, such as accidental death or critical illness coverage.

Wrapping Up

navigating the world of life insurance can be daunting, but understanding its fundamental aspects can empower you to make informed decisions for yourself and your loved ones. By grasping the importance of selecting the right coverage, understanding policy types, and recognizing the factors that influence premiums, you can tailor a plan that meets your unique needs. Remember, life insurance isn’t just a financial product; it’s a vital part of your overall financial strategy aimed at providing security and peace of mind. As you embark on this journey, consider consulting with a financial advisor to further clarify your options and ensure you choose the best path forward. Stay informed, ask questions, and take control of your financial future. Your family will thank you for it.